Forget what you know about personal loans or credit cards. Student loan repayment in the UK isn’t about fixed monthly instalments or the pressure to clear your balance as fast as possible. Instead, the system is designed to be much more flexible: what you pay back is based entirely on what you earn, not the total amount you actually borrowed.

Repayments only start once your income crosses a certain threshold, and they’re taken automatically from your pay, so you don’t have to worry about a thing. Interestingly, for many graduates, the loan is never fully repaid before it is written off. It often surprises people, but that’s actually a key part of how the system is designed to work.

UK Student Loan Repayment: An Overview

If you’re in a rush, here’s what you need to know about student loan repayment in the UK.

| Question | Key Answer |

| When do repayments start? | From the first April after you finish/leave your course — and only once income crosses your plan’s threshold (£25,000–£33,795/year, depending on plan) |

| How much do you repay? | 9% of income above the threshold (6% for Postgraduate Loans). If repaying two loans, each is deducted separately against its own threshold |

| How is it collected? | Automatic — via PAYE (shown on payslip) if employed, or via Self Assessment if self-employed/other income. No forms needed |

| Does interest accrue? | Yes, from the day the loan is taken out, continuously, regardless of whether repayments are being made. Rate varies with inflation |

| Can you repay early? | Yes, lump sum or extra payments, no penalty — but most Plan 2/5 borrowers weren’t on track to clear the balance before write-off anyway, so extra payments may be wasted |

| Are loans written off? | Yes, automatically after 25–40 years (varies by plan) or at a fixed age for older loans. No application needed; doesn’t affect credit file |

| What if you move abroad? | Must notify the Student Loans Company; repayments switch to a fixed overseas threshold. Missing this risks interest penalties or debt collection |

| Where to check your balance? | Online account with the Student Loans Company — shows balance, plan type, interest rate, and repayment history |

Also Read: Updated Guide To The Cost Of Studying In The UK – 2026

How Does Student Loan Repayment in the UK Work?

The UK student loan system uses income-contingent repayment. That single idea explains most of what feels unusual about it:

Your repayment amount is tied entirely to your salary, not to how much you originally borrowed. That means a graduate who took out £45,000 and one who took out £15,000, on the same plan and earning the same salary, end up repaying exactly the same amount each month. It’s also worth noting that this happens automatically, so there’s nothing you need to schedule or remember to pay yourself.

Who actually collects the money, though, involves three different parties working together:

Who collects your repayments?

- PAYE — your employer calculates and deducts the repayment from your salary, just like tax and National Insurance.

- HMRC — processes the deduction and passes the funds on.

- Student Loans Company (SLC) — maintains your loan account, tracks your balance and interest, and is who you contact directly for overpayments or overseas repayment.

When Do You Start Paying Back Student Loan?

Repayments don’t start the moment you graduate. They start the following tax year, and only once you’re earning enough.

You’ll have a little breathing space after university. Even if you graduate or leave your course earlier in the year, student loan repayment in the UK usually begins from the following April, and only if you’re earning above the required income threshold.

Even once that April arrives, repayments still won’t begin unless your income has crossed your plan’s specific threshold, which ranges from £25,000 to £33,795 a year depending on which plan applies to you. If your salary is below that figure, repayment doesn’t start yet, no matter how long it’s been since you left your course.

When you start earning money beyond this point, the deductions will happen automatically without requiring you to do anything. There is nothing that you have to arrange, request, or monitor. As soon as your earnings meet the criteria, the system takes over.

Thus, in case you will be graduating from college in June 2026, your repayment period will commence in April 2027, and the deduction will begin only after your salary exceeds the threshold.

Exceptions worth knowing

- If you are self-employed, you will not be paying back through PAYE. You will make your payments through Self-Assessment along with any repayment you need to make on your student loan.

- If your income dips below the threshold at any point (redundancy, career break, part-time work), repayments simply pause. Nothing is owed for that period.

- In case you are employed by more than one firm, each company considers the salary it pays you. This means deductions may sometimes be under or overcollected and later adjusted by HMRC.

- One-time payments like bonuses may lead to a temporary increase in monthly pay, which will result in a deduction for this particular month even though your annual salary is below the limit.

UK Student Loan Repayment Plans & Thresholds

Which plan you’re on depends on where in the UK you studied and when your course started. This determines both your threshold and how long until any remaining balance is written off.

| Plan | Who it’s for | Repayment rate | Salary threshold | Write-off |

| Plan 1 | Students from England/Wales who started before Sept 2012; all Northern Ireland students | 9% | £26,900/year | 25 years after your first April due to repay (or age 65 for pre-2006 loans) |

| Plan 2 | Students from England/Wales who started between Sept 2012 and July 2023 | 9% | £29,385/year | 30 years after your first April due to repay |

| Plan 4 | Scottish students (via SAAS) | 9% | £33,795/year | 30 years after your first April due to repay |

| Plan 5 | Students from England who started from Aug 2023 onwards | 9% | £25,000/year | 40 years after your first April due to repay |

| Postgraduate Loan | Master’s and Doctoral loan borrowers | 6% | £21,000/year | 30 years after your first April due to repay |

Plan 1

Plan 1 applies to students from England and Wales who started their course before September 2012, as well as all Northern Ireland students regardless of start date. You repay 9% of any income above £26,900 a year, and whatever balance remains outstanding is written off 25 years after your first April due to repay, or at age 65 if you took out the loan before 2006.

Plan 2

This plan covers students from England and Wales who started their course between September 2012 and July 2023. Repayments are 9% of income above £29,385 a year, a threshold that’s now frozen at this level until April 2030. Any remaining balance is cancelled 30 years after your first April due date.

Plan 4

Plan 4 is for Scottish students who borrowed through SAAS. You repay 9% of income above £33,795 a year, the highest threshold of any plan, and your balance is written off 30 years after your first April due date.

Plan 5

Plan 5 applies to students from England who started their course in August 2023 or later. It has the lowest threshold of any plan at £25,000 per year, with 9% repaid above that amount. It also has the longest student loan write-off period of any plan, at 40 years after your first April due to repay.

Postgraduate Loan

The Postgraduate Loan covers borrowers of the Master’s and Doctoral loans. It’s repaid at a lower rate of 6%, but on a much lower threshold of £21,000 a year. If you’re also repaying an undergraduate loan, both are deducted in parallel against their own thresholds. The remaining balance is written off 30 years after your first April due to repay.

Also Read: Cost of Living in London for Students

How Much Will You Repay?

Rather than working through formulas, it’s easier to see student loan repayment in the UK in action across a few salary levels. Remember: only the amount above your threshold is ever counted.

| Annual Salary | Repayment Plan | Monthly Repayment | Annual Repayment |

| £25,000 | Plan 5 | £0 | £0 |

| £30,000 | Plan 2 | £4.61 | £55.35 |

| £40,000 | Plan 1 | £98.25 | £1,179.00 |

| £60,000 | Plan 4 | £196.54 | £2,358.45 |

A higher salary doesn’t tell the whole story — the size of your threshold, which depends on your plan, changes the repayment just as much. Two people earning the same salary but on different plans can pay very different amounts.

Student Loan Repayment Calculator

Repayment = (Salary − Threshold) × Applicable repayment rate

Worked example: Plan 2, salary of £35,000

● Threshold: £29,385

● Amount above threshold: £35,000 − £29,385 = £5,615

● Repayment rate: 9%

● Annual repayment: £5,615 × 9% = £505.35

● Monthly repayment: £505.35 ÷ 12 ≈ £42.11

That £42.11 a month is what actually gets deducted from payslips, not 9% of the full £35,000 salary, which is where most of the confusion around student loan repayment comes from.

Just as choosing the right AI tool can make studying easier, finding the right student accommodation can transform your university experience. Explore verified and affordable student homes with UniAcco, including fully furnished studios, en-suite rooms, and shared apartments with all-inclusive bills, modern amenities, and flexible booking options near top universities.

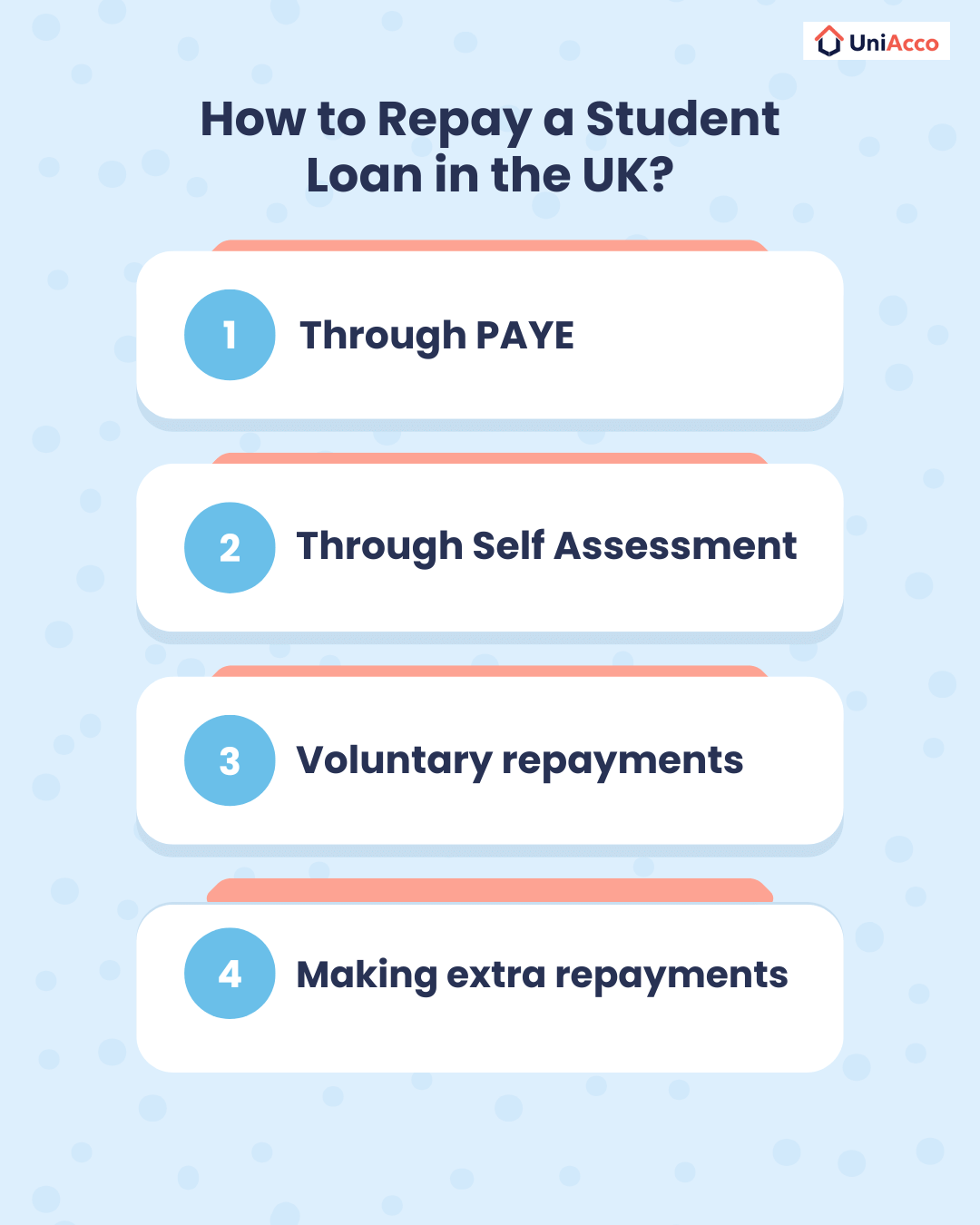

🔍 Explore Student AccommodationHow to Repay a Student Loan in the UK?

Through PAYE

For most of us who work, the entire process is quite hands-off. As soon as your income exceeds the amount needed to repay the loan, your employer takes care of the deductions from your salary before they reach your bank account. It will be easy for you to identify it as a separate line in your monthly paycheck.

Through Self Assessment

If you’re self-employed, or have income HMRC doesn’t see through PAYE, you declare it in your tax return, and any student loan repayment in the UK is calculated and paid alongside your Income Tax and National Insurance bill.

Voluntary repayments

You can make one-off or regular extra payments directly to the Student Loans Company at any time, on top of what’s deducted automatically, with no early repayment penalty.

Making extra repayments

For most Plan 2 and Plan 5 borrowers, your monthly payroll deduction stays exactly the same whether you overpay or not — extra payments just shrink the balance that would otherwise have been written off for free, meaning you end up paying more overall, not less.

Also Read: Top UK Bank Accounts for International Students

Repaying From Outside the UK

- Moving abroad doesn’t cancel your obligation to repay. It just changes how repayments are collected, since PAYE no longer applies.

- Update your contact details with the Student Loans Company as soon as you know your move-out date and new address.

- Declare the country you’re moving to, since overseas repayment thresholds are set on a country-by-country basis rather than using the UK threshold.

- Provide income evidence each year, so the SLC can work out your repayments based on your local salary.

- Set up a repayment method directly with the SLC, typically a direct debit from your UK student bank account or an international equivalent in the relevant currency, since deductions can no longer happen automatically through an employer.

Should You Repay Your Student Loan Early?

There’s no one-size-fits-all answer to early student loan repayment in the UK. If you’re earning enough to pay off the loan in full, paying extra can reduce the interest you pay and help you become debt-free sooner. On the other hand, many graduates on Plan 2 or Plan 5 won’t repay the entire balance before it’s written off, which means overpaying may not always be the smartest financial move. Before making additional payments, consider other priorities such as savings, investments, or paying off higher-interest debt. Once you’ve made a voluntary overpayment, you usually can’t get that money back.

Decision Matrix on Early Student Loan Repayment

| Situation | Usually Worth Paying Early? |

| High earner, on track to clear the balance well before write-off | Maybe |

| Average salary, especially on Plan 2 or Plan 5 | Usually not |

| Planning to apply for a mortgage soon | Depends on lender treatment of the debt |

| Moving abroad long-term | Depends on the overseas threshold and your income |

Conclusion

Student loan repayment in the UK behaves less like a debt and more like an extra rate of income tax that applies once you earn above a certain threshold, and disappears entirely after a set number of years. Knowing your plan, your threshold, and your student loan write-off date is really all you need to make sense of what’s coming out of your payslip each month, and whether there’s any real benefit to paying more than you have to.

If you’re planning your finances around your student loan, whether that’s budgeting for student living expenses and repayments in the UK, deciding on a mortgage application, or weighing up an overseas move, start by confirming your exact plan and threshold on your Student Loans Company account, since that’s the figure everything else in this guide is based on.

LinkedIn

LinkedIn

{kind=link}

0 Comments